Four years ago, when my wife and I were preparing to buy our first home, our income was limited and we were desperate to save as much money as we could. I had heard that there were tax benefits to purchasing a home, but I honestly knew very little info beyond that. But during my research, I stumbled across something called the MCC Tax Credit (Mortgage Tax Credit Certificate).

When I began to understand what it was, and why, for many people, it was a significantly better mortgage interest tax benefit than the mortgage interest deduction, I was surprised to find that very few people seemed to be talking about it online. Yet, despite the relatively light amount of information guiding our way, we were able to take advantage of this amazing tax perk.

Before we begin, let me say that it is not necessarily “easy” to set yourself up to earn the MCC Tax Credit on your annual tax return. It’s going to take some work and a little persistence. But, for those in the right situation, a little extra work could literally save you up $2,000 a year…for the life of your loan!

Let’s begin by examining the difference between the MCC and the more widely-known mortgage interest deduction.

The Key Is in the “Credit”

The Tax Cuts and Jobs Act of 2017 nearly doubled the standard deduction. Couples that are married filing jointly, for instance, now have a standard deduction of $24,400. This will, of course, lead to many more families taking the standard deduction as opposed to itemizing their deductions. And, if you’re not itemizing your deductions, then the mortgage interest deduction is of no benefit to you.

But, the MCC is also a tax benefit based off of the mortgage interest that you pay, and it does not suffer in any way from the new tax law. In fact, it may be one of the only tax benefits that are still a viable option for a large majority of homebuyers. To understand why you need to understand the difference between a tax credit and a tax deduction.

What Are Tax Deductions?

A tax deduction lowers the amount of your income that you are allowed to be taxed on. For example, if you make $50,000 a year, and you have $10,000 of deductions, you are only allowed to be taxed on $40,000. So, instead of owing $6,939 in tax, you would only owe $4,739.28.

But, again, with the new tax law, your taxable income is already being automatically dropped $12,000 for single filers and $24,000 for couples filing jointly by the standard deduction. You cannot add more deductions to the standard deduction. You can either take the standard deduction, or you can choose to itemize. If your total deductions (home-related, work-related, and charity-related deductions, all added together) do not exceed the standard deduction, then you should not itemize. Unfortunately, the moment you choose to forgo itemizing, the mortgage interest deduction becomes useless to you, along with every other deductible expense that you may have accumulated throughout the year.

What Are Tax Credits?

Tax credits are a completely different beast, however. As opposed to lowering your taxable income, tax credits actually subtract from the amount of tax that you owe. This is what makes the MCC such a fantastic deal! If, let’s say, after taking the standard deduction, you still owe $5,000 in taxes, the MCC could drop that tax bill by $2,000 – making your tax bill $3,000 instead of $5,000.

Do you see the big difference? A $2,000 deduction, would only change your tax bill a few hundred dollars, at best; but a $2,000 credit is an actual $2,000 in your pocket! It’s truly a dollar-for-dollar credit to increase home affordability. And the best part – even if you do happen to be someone who itemizes your deductions, and you receive a deduction for your mortgage interest, you can still claim this credit!

Who Is Eligible for the MCC Tax Credit?

In order to qualify for the MCC Tax Credit, you’ll need to meet the eligibility criteria. As detailed below, you’ll need to be a first-time home buyer and you’ll need to meet your state’s income and home purchase price limits.

First-Time Home Buyers

The MCC program was put in place by the government, as a way to give assistance and relief to first-time home buyers. If you’re someone who has already bought your first home, unfortunately, you’re most likely out of luck. However, there are some exceptions:

- The state HFA’s (Housing Finance Agencies) define a new home buyer as being someone who has not had an ownership principal in a residence in 3 years. So, if you bought a home in the past, but have not owned a home in the past 3 years, you can qualify for the MCC.

- The first-time homebuyer requirement is waived for borrowers purchasing a home in targeted areas as defined by (HUD) at the census tract level or designated by state governments. To find your state’s targeted areas, click on the link to your state’s MCC guide at the bottom of this article.

- The first-time homebuyer requirement is waived for active military and veterans.

Income Limits

Every county in each state has a different maximum income limit for qualifying the MCC. Again, links can be found at the end of this article for your state’s guidelines. Where I live in Volusia County (which is one of the poorer counties in Florida), here are the income limits:

- Non-Targeted Area:

- 1-2 person household – $63,766

- 3+ person household – $73,311

- Targeted Area:

- 1-2 person household – $75,000

- 3+ person household – $87,500

For Broward County, which happens to be one of the wealthier counties in Florida, the numbers look like this:

- Non-Targeted Area:

- 1-2 person household – $80,800

- 3+ person household – $92,920

- Targeted Area:

- 1-2 person household – $96,960

- 3+ person household – $113,120

Again, every county will be different. But this gives you an idea of the range that the MCC income limits will tend to fall within.

Price Limits

There is a limit to how expensive of a home you can purchase and still qualify for the MCC. To give you an idea of what you may be looking at, I’ve used the same sample Florida counties as above.

- Volusia County

- Non-Targeted Area – $271,165

- Targeted Area – $331,423

- Broward County

- Non-Targeted Area- $317,647

- Targeted Area- $388,235

Honestly, I find both the income and price limits to be quite reasonable, unlike many other government-sponsored programs that very few middle-class families can qualify for.

How Do You Calculate How Much Credit You Can Claim?

The amount of credit you can claim is based off a percentage of the mortgage interest that you paid during the previous year. The percentage can fall anywhere between 10 and 50 percent. The more expensive the home purchase, the lower the percentage will be.

Let’s say you qualified to receive a credit of 50 percent of your mortgage interest paid (as my wife and I did), and let’s take a look at an oversimplified home purchase, for sake of illustration.

- Loan Amount – $100,000

- Interest Rate – 4.5%

- Total Mortgage Interest Paid Year 1 – $4,467

- 50 Percent of Mortgage Interest Paid– $2,233

- Total Credit Earned – $2,000 (the maximum that can be applied to one year’s tax bill)

As you can see, in the above scenario, the home buyers earned the full $2,000 max tax credit.

How Long Can the Credit Be Applied?

For the life of the loan! Yes, you read that right.

Now, as time moves forward, and as the home buyers in our example continue to make mortgage payments, their payments will increasingly be going towards principal, and less towards interest.

So, eventually, their annual mortgage interest paid for the year will dip below $4,000 and they will earn less than the $2,000 max. But until the home is sold or paid off in full, the credit can be claimed. This means that homeowners could literally save tens of thousands of dollars through taking advantage of this program!

Choosing an MCC-Approved Lender

Somewhat surprisingly, you do not have to buy your home via an FHA loan in order to qualify for the MCC. All first mortgage loan types are eligible (FHA, VA, RHS, and Conventional).

Where things get a bit more difficult is when it comes to choosing your lender. You can only qualify for the MCC if you use an MCC-approved lender. You can find a list of your state’s approved lenders on your state’s MCC guide.

Unfortunately, if you live in a smaller town, there’s a good chance you may have no local lenders who are MCC-approved. My wife and I actually live in a fairly large town; yet, the closest MCC-approved lender to us was in Orlando, which is about an hour away from where we live.

Hiring an Out-of-Town MCC-Approved Lender (It’s Ok, Really!)

Our real estate agent was not too happy to find out that we were planning to use an Orlando lender for our home purchase. Real estate agents usually have their 2 or 3 local lenders that they like to work with. Out-of-town lenders can worry agents because they add an element of “unknown” to the process.

- What if the lender is hard to work with?

- What if there are unnecessary delays and the loan is not ready by the closing date?

- What if the lender decides to deny the loan even though they have said that it’s already been “pre-approved.”

I understood my agent’s concern, but I remained firm that we had to use this lender. I tried to explain why, but my agent had never heard of the MCC tax credit before with any of her previous clients (don’t be surprised if your real estate hasn’t heard of it either).

To be honest, I think she thought I was a little bit crazy. But I was undeterred. I stuck with my guns, and I’m glad that I did, because it has literally saved us thousands of dollars.

With many lenders, there is an extra fee they add on to the loan for those who apply for the MCC. In our case, the fee was around $600. This fee was added to our closing costs. This may seem like a lot of money, but I knew we’d make up that cost on our first tax return alone, with an extra $1,400 to spare. And then every following year would just be additional free money!

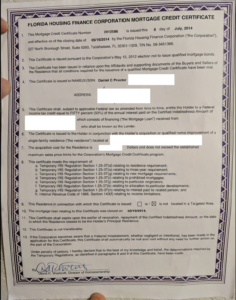

Soon after you’ve been approved for the MCC, you’ll receive a letter that looks like this, letting you know you’re all set!

You Must Apply for the MCC Tax Credit Before Buying Your Home

Some of you may be sitting on your couch right now and you’re thinking to yourself, “Hey, I’m still in my first home! I’m going to apply for this thing!” Sadly, once your home purchase is complete, you are no longer eligible for the MCC. You must get yourself set up for it before you buy your home! If you know someone who’s getting ready to buy a home, don’t delay to tell them about the MCC. Literally, a day after they’ve bought their home, they will no longer be eligible.

This rule also applies to refinance loans. If the original loan did not include the MCC tax credit, you cannot add it during the refinance process. However, if you do have an MCC on your current loan and decide to refinance, you can apply to receive a new MCC issued against your refinanced mortgage.

Related: How Long Does the Home Closing Process Take?

How to Claim the MCC Tax Credit on Your Tax Return

For those of you who use a tax software program, each of them should have a section where they ask you about the MCC. I happen to use TurboTax, and they take care of everything automatically, including calculating the exact amount of credit that I will receive.

If you are someone who happens to still do paper tax returns, then you will need to fill out Form 8396.

“Non-Refundable” Tax Credit

It should be noted that the MCC is a non-refundable tax credit. With refundable tax credits, even if your tax liability is $0, you still receive the full amount of the tax credit in the form of a refund.

With non-refundable tax credits, however, the credit can only be used to bring your tax liability down to $0. What this means is that if, after your deductions and credits, you owe little to no income tax, the MCC may not be very useful to you.

What If I Claim the Mortgage Interest Deduction?

As I mentioned earlier in the article, you can still benefit from the MCC tax credit even if you’re someone who does claim the mortgage interest deduction on your taxes. Yes, you can actually combine the two benefits together.

All you have to do is take however much of an MCC credit you received and subtract that amount from your mortgage interest deduction.

Let’s say you paid $5,000 in mortgage interest during the previous year. If you lived in a state where you could claim 50% of your mortgage interest as a credit, you would receive the full $2,000 credit. Therefore, you would subtract $2,000 from your mortgage interest deduction total, claiming $3,000 as opposed to $5,000.

In summary, you could:

- Claim a $2,000 MCC tax credit, AND

- Claim a $3,000 mortgage interest deduction

Pretty incredible, right? Again, I know the math may seem a little complicated, but if you use an electronic tax software for your taxes, most will already have all these rules programmed in and will automatically combine the two benefits together for you.

Recapture Tax: Unlikely to Be a Problem, But Something to Be Aware Of

On the FDIC’s MCC guide, they explain that a borrower can owe a “recapture tax” on the resale of their home, if they meet all 3 of the criteria below:

- The borrower sells the home within nine years of purchase.

- The borrower earns significantly more income than when he/she bought the home.

- The borrower has a gain from the sale of the home.

If all 3 of these circumstances were to take place, your state could require that you pay up to 6.25 percent of the original principal balance of the loan or 50 percent of the gain on the sale of the home, whichever is less.

The FDIC guide is quick to note that most state’s housing agencies report that the majority of their program recipient’s have not been subject to tax recapture. However, if you have a feeling that there’s a good chance you may meet all 3 of the above criteria when you sell your home, it may be a reason for you to stay away from the MCC.

State MCC Guides

To find details for your specific state, you’ll find a link to each state’s guide below. Please click on the state you are interested in to view that state’s information:

- Alabama

- Alaska

- Arizona

- California

- Colorado

- Connecticut

- Deleware

- Florida

- Georgia

- Hawaii

- Idaho

- Illinois

- Indiana

- Iowa

- Kansas

- Kentucky

- Louisiana

- Maine

- Maryland

- Massachusetts

- Michigan

- Minnesota

- Mississippi

- Missouri

- Montana

- Nebraska

- Nevada

- New Hampshire

- New Jersey

- New Mexico (does not participate in the MCC program, but does have a different one called the Affordable Housing Tax Credit Program)

- New York

- North Carolina

- North Dakota (does not participate)

- Ohio

- Oklahoma

- Oregon

- Pennsylvania

- Rhode Island

- South Carolina

- South Dakota

- Tennessee

- Texas

- Utah

- Vermont

- Virginia

- Washington

- West Virginia

- Wisconsin

- Wyoming

Great guide. I took was surprised by how little literature exists online about the benefit. Only thing I’d add here is either a section on or link to info on how to adjust W4s to ensure full benefit is claimed due to non-refundability.

Thanks, for the compliment Joey.

That’s a great point about adjusting W4s if you have years of non-refundability. I think many of the tax software companies will do that for you (I know TurboTax does for me), but it would definitely be worth adding in a section on that for people who do their taxes themselves. I’ll try to add that in soon.

Thanks for the idea!

Clint